All Categories

Featured

Table of Contents

That usually makes them a much more budget friendly alternative for life insurance protection. Some term policies might not maintain the costs and survivor benefit the very same in time. You don't intend to erroneously assume you're purchasing degree term protection and afterwards have your survivor benefit adjustment in the future. Numerous individuals obtain life insurance policy protection to help financially safeguard their enjoyed ones in situation of their unexpected death.

Or you might have the option to transform your existing term protection right into a long-term policy that lasts the remainder of your life. Various life insurance policy plans have potential benefits and disadvantages, so it's vital to understand each before you choose to purchase a plan.

As long as you pay the costs, your recipients will obtain the survivor benefit if you pass away while covered. That said, it is necessary to keep in mind that a lot of policies are contestable for two years which implies coverage can be retracted on fatality, ought to a misstatement be located in the application. Policies that are not contestable usually have actually a rated survivor benefit.

Premiums are generally lower than entire life plans. You're not secured right into an agreement for the rest of your life.

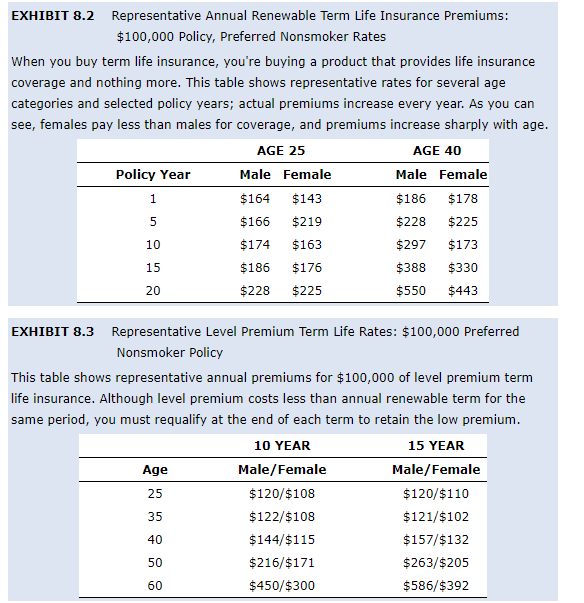

And you can not cash out your policy during its term, so you won't get any type of financial gain from your previous insurance coverage. Just like other kinds of life insurance coverage, the price of a level term plan relies on your age, protection demands, employment, way of living and wellness. Commonly, you'll discover more cost effective coverage if you're more youthful, healthier and much less dangerous to guarantee.

A Whole Life Policy Option Where Extended Term Insurance Is Selected Is Called

Considering that level term premiums remain the same for the duration of insurance coverage, you'll understand precisely how much you'll pay each time. Level term coverage additionally has some flexibility, allowing you to personalize your policy with added features.

You might have to satisfy particular problems and qualifications for your insurance provider to enact this rider. There additionally can be an age or time limitation on the insurance coverage.

The death benefit is generally smaller sized, and insurance coverage typically lasts up until your youngster turns 18 or 25. This rider might be a more cost-effective way to assist ensure your youngsters are covered as motorcyclists can typically cover multiple dependents at when. When your kid ages out of this insurance coverage, it might be feasible to transform the motorcyclist right into a brand-new policy.

When comparing term versus permanent life insurance. short term life insurance, it is very important to keep in mind there are a couple of different kinds. The most usual kind of long-term life insurance policy is entire life insurance coverage, yet it has some crucial differences contrasted to level term coverage. Below's a standard introduction of what to take into consideration when comparing term vs.

Entire life insurance coverage lasts for life, while term insurance coverage lasts for a certain period. The premiums for term life insurance policy are usually lower than entire life coverage. With both, the costs continue to be the very same for the period of the plan. Whole life insurance policy has a cash money value part, where a part of the costs may grow tax-deferred for future requirements.

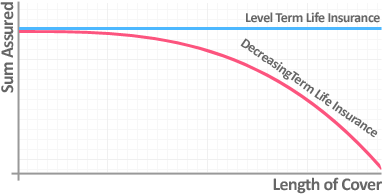

Among the highlights of level term insurance coverage is that your costs and your death advantage don't alter. With lowering term life insurance, your premiums remain the same; nevertheless, the death benefit quantity obtains smaller sized in time. You might have insurance coverage that starts with a fatality advantage of $10,000, which could cover a home loan, and after that each year, the fatality advantage will lower by a collection amount or percentage.

Due to this, it's typically an extra cost effective sort of level term coverage. You might have life insurance policy via your employer, but it might not suffice life insurance policy for your demands. The very first step when acquiring a plan is establishing just how much life insurance policy you need. Consider aspects such as: Age Household size and ages Work standing Earnings Financial obligation Way of living Expected last expenses A life insurance coverage calculator can help establish just how much you require to begin.

After deciding on a policy, finish the application. If you're accepted, authorize the paperwork and pay your first premium.

Innovative Term Life Insurance With Accidental Death Benefit

Finally, take into consideration scheduling time yearly to examine your policy. You might want to update your beneficiary info if you've had any type of substantial life changes, such as a marital relationship, birth or divorce. Life insurance can often really feel complicated. But you don't have to go it alone. As you discover your choices, consider reviewing your demands, desires and concerns with a monetary expert.

No, degree term life insurance policy does not have cash money value. Some life insurance policy plans have a financial investment function that allows you to construct money value over time. A section of your premium settlements is established aside and can make interest with time, which grows tax-deferred during the life of your insurance coverage.

Nonetheless, these policies are frequently substantially a lot more expensive than term insurance coverage. If you get to completion of your policy and are still alive, the insurance coverage ends. Nevertheless, you have some choices if you still desire some life insurance policy protection. You can: If you're 65 and your coverage has gone out, for instance, you might intend to acquire a new 10-year level term life insurance coverage policy.

Premium Decreasing Term Life Insurance Is Often Used To

You might be able to transform your term insurance coverage right into an entire life plan that will certainly last for the remainder of your life. Lots of sorts of level term policies are exchangeable. That means, at the end of your protection, you can transform some or every one of your plan to whole life coverage.

Degree term life insurance policy is a plan that lasts a collection term normally in between 10 and thirty years and comes with a degree fatality advantage and degree costs that remain the exact same for the entire time the policy is in effect. This implies you'll know precisely just how much your payments are and when you'll have to make them, enabling you to budget as necessary.

Level term can be a terrific option if you're aiming to purchase life insurance protection for the first time. According to LIMRA's 2023 Insurance Measure Research, 30% of all adults in the United state requirement life insurance and don't have any kind of kind of plan. Level term life is foreseeable and cost effective, which makes it among one of the most popular kinds of life insurance.

{kind=link}

Latest Posts

Best Funeral Plans For Over 50s

Burial Insurance Quote

Burial Life Insurance Policies