All Categories

Featured

Table of Contents

There is no payout if the plan runs out before your fatality or you live beyond the policy term. You might have the ability to renew a term plan at expiry, however the costs will certainly be recalculated based upon your age at the time of renewal. Term life insurance is generally the the very least pricey life insurance policy readily available because it provides a fatality advantage for a limited time and doesn't have a cash money worth part like irreversible insurance coverage.

At age 50, the premium would certainly climb to $67 a month. Term Life Insurance Policy Rates thirty years old $18 $15 40 years old $28 $23 50 years old $67 $51 Source: Quotacy. Quotes are for a $250,000 30-year term life plan, for males and females in excellent health and wellness. In contrast, below's a take a look at prices for a $100,000 entire life policy (which is a type of irreversible plan, meaning it lasts your life time and consists of cash money worth).

The minimized risk is one aspect that enables insurance companies to bill reduced premiums. Rate of interest, the financials of the insurance provider, and state policies can additionally affect costs. Generally, business typically supply far better rates at the "breakpoint" coverage levels of $100,000, $250,000, $500,000, and $1,000,000. When you take into consideration the quantity of protection you can get for your premium bucks, term life insurance coverage often tends to be the least expensive life insurance policy.

He acquires a 10-year, $500,000 term life insurance plan with a costs of $50 per month. If George dies within the 10-year term, the policy will pay George's recipient $500,000.

If George is diagnosed with an incurable illness throughout the very first policy term, he probably will not be eligible to restore the plan when it ends. Some policies use assured re-insurability (without evidence of insurability), however such attributes come with a higher cost. There are a number of types of term life insurance coverage.

Many term life insurance has a degree premium, and it's the type we have actually been referring to in most of this write-up.

Does Term Life Insurance Cover Accidental Death

Term life insurance policy is eye-catching to young people with children. Parents can get considerable insurance coverage for an inexpensive, and if the insured passes away while the policy is in effect, the household can count on the fatality advantage to change lost revenue. These policies are likewise fit for individuals with expanding households.

The ideal choice for you will depend upon your needs. Below are some points to consider. Term life plans are ideal for individuals that want significant coverage at an inexpensive. Individuals that own entire life insurance policy pay a lot more in premiums for much less coverage but have the safety of knowing they are safeguarded permanently.

The conversion rider ought to allow you to transform to any kind of long-term policy the insurance policy company offers without constraints. The primary functions of the rider are preserving the original health score of the term policy upon conversion (even if you later on have wellness issues or become uninsurable) and making a decision when and just how much of the insurance coverage to convert.

Naturally, overall costs will increase significantly considering that entire life insurance policy is extra costly than term life insurance. The advantage is the guaranteed approval without a medical examination. Medical conditions that establish during the term life duration can not trigger costs to be enhanced. The firm might require limited or full underwriting if you want to include additional bikers to the brand-new policy, such as a long-lasting care cyclist.

Term life insurance policy is a fairly affordable means to supply a round figure to your dependents if something happens to you. It can be a good option if you are young and healthy and support a household. Entire life insurance policy comes with considerably greater month-to-month premiums. It is indicated to give coverage for as lengthy as you live.

Sought-After What Is Direct Term Life Insurance

It depends upon their age. Insurance policy companies set an optimum age limitation for term life insurance policy policies. This is generally 80 to 90 years of ages yet may be greater or reduced depending upon the company. The premium likewise increases with age, so a person aged 60 or 70 will certainly pay considerably even more than someone decades more youthful.

Term life is rather comparable to auto insurance coverage. It's statistically not likely that you'll require it, and the premiums are money down the tubes if you don't. If the worst occurs, your household will get the benefits.

One of the most preferred type is currently 20-year term. Most business will not offer term insurance coverage to an applicant for a term that ends past his/her 80th birthday celebration. If a plan is "eco-friendly," that suggests it continues in pressure for an additional term or terms, approximately a defined age, also if the health and wellness of the insured (or various other variables) would cause him or her to be declined if he or she looked for a new life insurance policy plan.

So, premiums for 5-year renewable term can be level for 5 years, after that to a new rate showing the new age of the insured, and so forth every five years. Some longer term plans will assure that the costs will not increase during the term; others do not make that warranty, enabling the insurer to elevate the price throughout the plan's term.

This suggests that the policy's proprietor deserves to transform it right into a long-term sort of life insurance coverage without extra evidence of insurability. In many kinds of term insurance policy, including house owners and automobile insurance coverage, if you have not had a claim under the policy by the time it runs out, you get no refund of the premium.

Comprehensive What Is Direct Term Life Insurance

Some term life insurance policy customers have actually been dissatisfied at this outcome, so some insurance firms have developed term life with a "return of premium" feature. term to 100 life insurance. The premiums for the insurance with this attribute are commonly considerably more than for policies without it, and they normally call for that you keep the policy in pressure to its term otherwise you surrender the return of premium advantage

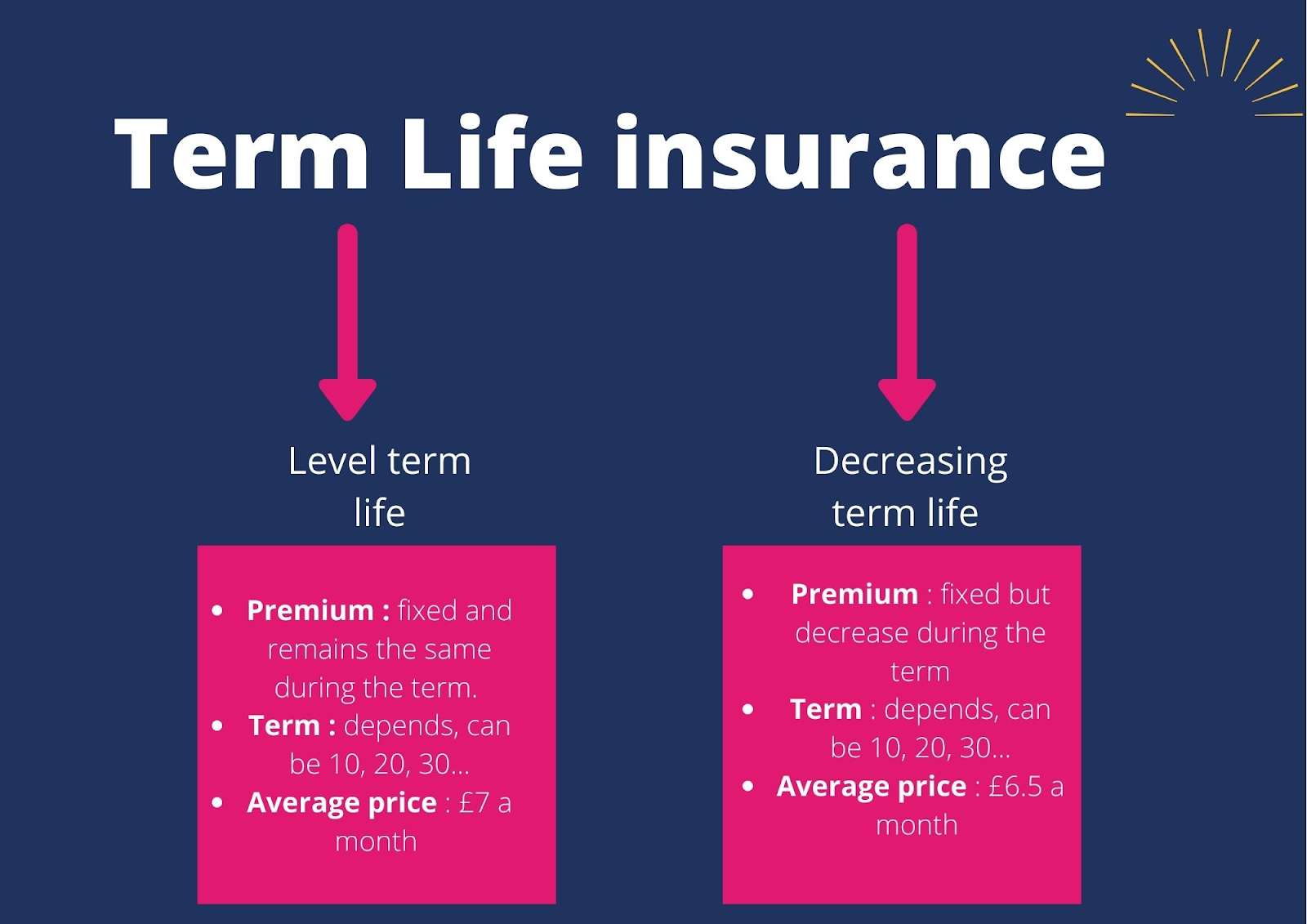

Degree term life insurance policy premiums and fatality benefits remain regular throughout the policy term. Degree term plans can last for periods such as 10, 15, 20 or 30 years. Level term life insurance coverage is usually much more budget friendly as it does not construct cash money value. Degree term life insurance policy is one of one of the most common types of protection.

Exceptional What Is Decreasing Term Life Insurance

While the names typically are utilized interchangeably, degree term insurance coverage has some vital differences: the costs and death benefit remain the very same throughout of protection. Degree term is a life insurance policy policy where the life insurance coverage premium and survivor benefit stay the same throughout of protection.

{kind=link}

Latest Posts

Best Funeral Plans For Over 50s

Burial Insurance Quote

Burial Life Insurance Policies